Mark-to-Market Example

We will present two broad overview examples. One will exhibit the tax benefits of the MTM election whereas the second will show the potential detrimental impact of the election.

Note: These are two separate examples shown using the same security (SPX) so each example is a stand-alone scenario, not cumulative.

Example 1: Trader purchases 100 shares of SPX on 3/10/2008

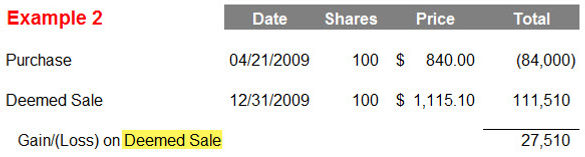

Example 2: Trader purchases 100 shares of SPX on 4/21/2009

Example 3: Continuing Example 1 with a subsequent sale

Example 4: Continuing Example 2 with a subsequent sale

Assumption: Trader made a timely and effective MTM election prior to tax year 2008.

This example also uses a stock index instead of an ETF or single stock. Thus the gain or loss when trading the index itself is reported on Form 4797, Part II while gain or loss on options on the index is reported on Form 6781. If this had been an ETF or single stock, it would also be reported on Form 4797, Part II as well.

Note ...

I have used the crash of 2008 and mini-2009 recovery as the example for the MTM Election - even though somewhat dated - because it provides the perfect scenario for BOTH a positive and negative adjustment.

It also fully illustrates that the Mark-to-Market Election decision is not to be taken lightly.

What you will notice is that the opposite market movement could also occur. For example, the SPX could close at an historical high on 12/31 but crash in subsequent months, much like what happened at the beginning of 2016.

Essentially, the trader is required to mark-to-market all gains but when the tax return comes due and the market has declined, there may be a cash shortage if depending on the previously marked to market securities to pay the tax.

SPX chart for 2008 and 2009

Example 1

Deemed sale results in a significant loss. For a MTM Trader this is reported on Form 4797 Part II.

Example 2

Deemed sale results in a significant gain. For a MTM Trader this is also reported on Form 4797 Part II.

Basis Adjustment

In Example 1, the new basis in the shares is adjusted for the loss recognized. Therefore, new basis per share is $903.25 and the holding period is short-term (Example 3).

Similarly, in Example 2, new basis is adjusted for the gain recognized. Thus, the new basis per share is $1,115.10 and the holding period is again, short-term (Example 4).

Example 3

New basis and holding period result from the MTM adjustment on 12/31/2008.

Example 4

New basis and holding period result from the MTM adjustment on 12/31/2009

Conclusion

As you can see, there is a tax benefit when a loss can be recognized. Unfortunately, this loss may no longer be carried back for two years to prior tax periods and offset any prior year capital gains. However, it can be carried forward indefinitely.

There is the potential for additional tax liability based on the deemed sale at a higher price. If you do not have the funds to pay the tax you may need to sell a position you do not want to sell as in Example 2 & 4.